By Marcus Webb | Personal Finance Advisor & Mortgage Planning Specialist May 2026 · 10 min read

I’ve been sitting across from many people who just took out a loan and knew nothing about what they were actually going to be paying off.

We know that, it’s not the number of months. The thing they didn’t realize was that, on a 30-year loan with a 6% interest rate, they will end up paying nearly as much interest as they will actually borrow. All that was ever known. It was in the papers. But no one had introduced it to them like that, making it real.

An amortization calculator is just that. It calculates your loan amount, interest rate and loan term — and lets you know the truth. Every payment. All the interest on every dollar.All of the interest on all dollars. Each month you are making repayments. Not at the end as you might expect, but before you sign.

The Amortization Calculator is a step-by-step guide to how the Amortization Calculator works, what it does, and how to use the numbers it provides to make better borrowing decisions.

Advanced Amortization Calculator

What Is an Amortization Calculator?

An Amortization Calculator is a financial instrument that will calculate the complete repayment schedule of your loan.

You enter the 3 basic numbers:

- The figure of the loan amount (the amount you are borrowing).

- Annual interest rate

- The number of years to repay the loan (loan term).

And it gives you back:

- The exact amount you’ll have to pay each month

- The sum of the interest paid over the life of the loan.

- A fully detailed amortization schedule which shows all payments as both principal and interest

- Your balance will be calculated by subtracting the amount of your payment from your total owing.

This is a huge difference from knowing simply how much your monthly payment would be. Monthly payment allows you to know what is taken out of your account each month. The amortization schedule indicates where it actually goes — and, in the first few years of many loans, much of the money goes toward interest.

What Is an Amortization Schedule?

This is the most relevant information the calculator yields, and it is essential to comprehend it correctly.

An amortization schedule is a detailed repayment schedule that lists — for each individual payment over the life of your loan — how much of the principal and how much of the interest you’re paying and how much is left over after the payment.

The real value added is to the extent that the interest/principal split is not predetermined. Changes on a per-payment basis.

Most of the loan payment in the first years is for interest. Naturally, principal reduction takes a long time. Over the years, things change – your interest decreases as the principal decreases, and more of your payment is applied to the principal amount.

Simplified version of this:

| Payment # | Payment | Interest | Principal | Remaining Balance |

|---|---|---|---|---|

| 1 | $1,799 | $1,500 | $299 | $299,701 |

| 60 | $1,799 | $1,392 | $407 | $231,882 |

| 180 | $1,799 | $1,092 | $707 | $180,451 |

| 300 | $1,799 | $530 | $1,269 | $103,879 |

| 360 | $1,799 | $9 | $1,790 | $0 |

(Based on $300,000 loan, 6% rate, 30-year term)

See the difference between payment #1 and #360. The same amount of payment. Completely different allocation. At the start, $1,500 of your $1,799 goes to interest. The last payment, nearly all of it is a negative balance payment.

That’s why extra early payments really are so strong and that’s why there’s an extra payment feature on the calculator.

How the Calculator works — all features explained

Monthly Payment Calculator

The core function. Just enter in your loan amount, rate, and term and the calculator returns your exact monthly payment in the standard amortization formula.

The folks who don’t do what most people don’t do next, though, is examine the total interest figure next to it. On a $300,000 mortgage at 6% over 30 years, the monthly payment is about $1,799. Manageable. But total interest paid over 30 years is approximately $347,515. You borrowed $300,000 and you’ll pay back $647,515.

That number alters the decision. The idea is to see it clearly.

Mortgage Amortization Calculator

This is the most important planning tool for homebuyers before making an offer.

The mortgage amortization calculator works out:

- A table showing the different payment amounts and rates for various loan amounts, for a particular month.

- The sum of all the interest paid throughout the loan.

- A description of how the balance decreases over the years

- The effect of varying down payment amounts on long-term cost of the purchase

This calculation should be done before rather than after buying a house. It may seem like a minor monthly difference, but the difference between the $280,000 loan and the $320,000 loan is significant. Over 30 years at 6%, it’s about $40,000 in extra interest. Here is a number to be known in advance!

Loan Amortization Schedule

The complete amortized schedule of loan repayments. Every payment. Every month. Throughout the duration of the loan.

This is useful for:

- Knowing exactly how much your loan balance will be at any time in the future

- What percentage of your equity will you have at the end of the 5th, 10th or 20th year?

- To find the exact sum you will receive when you refinance or sell

- Ensuring lenders/advisors know what you are doing to pay back.

This table is viewed by very few people. Those who do make far superior choices for refinancing, additional payments, and loan comparison.

EMI Calculator

Equated Monthly Installment (EMI) is the same as a monthly payment but just rephrased, very commonly used for home loans, auto loans and personal loans in many countries.

The EMI calculator is based on:

- Principal amount

- Annual interest rate

- Term of the loan in months or years.

It will return the fixed monthly payment amount throughout the term of the loan.

The word to look for is fixed. The EMI doesn’t change from month to month; the amount the interest component and the principal component is what changes, and that is exactly what you see in the amortisation schedule.

Extra Payment Calculator — The Most Underused Feature

It’s one that has a more significant impact on the math than most borrowers realize.

Pay more, pay off more principal. The lower the principal, the lower the interest that will be charged each month. If you were to make only a small extra payment over the course of a 30-year mortgage, you could save tens of thousands of dollars and reduce the number of years it will take you to pay it off.

What you can expect to accomplish with extra mortgage payments of $300,000 at 6%:

| Extra Monthly Payment | Interest Saved | Years Saved |

|---|---|---|

| $0 (standard) | — | — |

| $50/month | ~$22,000 | ~2 years |

| $100/month | ~$40,000 | ~4 years |

| $250/month | ~$82,000 | ~8 years |

| $500/month | ~$130,000 | ~13 years |

These are just rough estimates — use your particular numbers in the calculator to get accurate results. However, the trend is evident: any additional payment made in the early months of a mortgage will have a disproportionate effect since the money will be applied to the principal balance due on each subsequent payment.

These savings are displayed directly on the calculator, not in terms of percentage or “saved in years” but in dollars and years. That’s the number you need to get people to behave differently.

Auto Loan Amortization Calculator

The financing of cars follows the same amortization as the financing of a house, but shorter terms and often smaller amounts.

If a car buyer is looking at two financing offers, such as 5.9% for 60 months or 4.9% for 48 months, they can then plug those amounts into the auto loan calculator and see not only how much more they will make in monthly repayments on the loan with the higher interest rate, but also how much more interest they will pay over the life of the loan. The lower rate, shorter-term loan may be more expensive per month, but be cheaper over the period of the loan.

It is not possible to make such a comparison in your head. The calculator makes it a 30 second exercise.

Balloon Payment Calculator

Balloon payment loans are a type of loan in which the borrower makes regular smaller payments over a specified period of time and then pays a large payment at the end of the loan – these are usually commercial loans and some mortgages.

This is more risky than a typical amortization loan, as the big final repayment may surprise borrowers if they aren’t ready for it. In the balloon payment calculator, you’ll see:

- The amount of each payment

- The amount of balloons that will be there

- When it comes due

- The appearance of the remaining balance as they get closer to the balloon date.

Before signing any loan with a balloon payment, this is something that you cannot afford to not do. That final payment is usually big enough that it needs to be refinanced and you want to know that going in, not when it’s there.

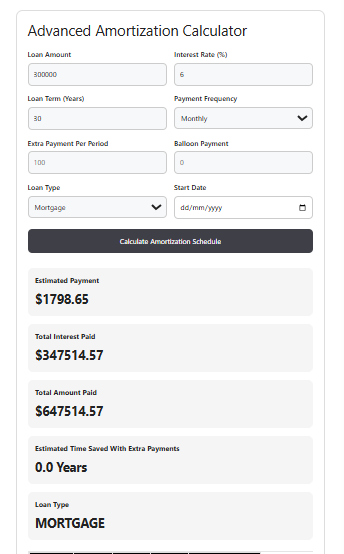

A Real Calculation — $300,000 Mortgage, 6%, 30 Years

Let me walk through a complete example so you can see exactly what the calculator produces.

Inputs:

| Field | Value |

|---|---|

| Loan Amount | $300,000 |

| Annual Interest Rate | 6% |

| Loan Term | 30 years |

| Extra Monthly Payment | $0 |

Results:

| Output | Amount |

|---|---|

| Monthly Payment | $1,798.65 |

| Total Interest Paid | $347,514.57 |

| Total Amount Paid | $647,514.57 |

| Loan Payoff Date | 30 years from start |

Now run the same loan with $200/month extra:

| Output | Standard | With $200 Extra |

|---|---|---|

| Monthly Payment | $1,798.65 | $1,998.65 |

| Total Interest | $347,514 | $263,816 |

| Interest Saved | — | $83,698 |

| Years Saved | — | ~6.5 years |

Two hundred dollars a month saved over $83,000 in interest and cut 6.5 years off the loan. That’s the kind of calculation that changes how people think about their mortgage.

Fixed vs Variable Interest Rates — Which to Calculate For

The amortization calculator can be used with variable and fixed rate loans, but the way to go about it is different.

Fixed Rate Loans

The interest rate does not change over the life of the loan. You never pay more for each month. You know exactly how much you’ll be paying down each month, in advance.

When you’re using the calculator to figure out a fixed rate loan, you will have a completely precise view of all future payments. As advertised, you get what you pay for.

Best for:

- Mortgages that require steady payments over an extended period of time

- Lenders who focus on consistency over optimization of their rates

- Anyone who wishes to be free from market conditions on their payment

Variable Rate Loans

This rate is adjusted periodically according to a reference rate. Payments may be positive or negative.

If the loan is variable, use your current rate and then use a higher scenario rate (2% higher than your current rate). A comparison of those two outputs will help you understand the amount of payment risk you are taking in the event of rates rising.

Best for:

- Loans with lower risk of rate adjustment and shorter terms of the loan.

- Borrowers considering selling or refinancing prior to a major rate increase

- When the first rate savings are significant.

How to Use the Calculator — Step by Step

Step 1 — Type Your Loan Amount The sum of the total money that you are borrowing. In the case of a home you are buying, it is the amount of money you pay for the house minus the down payment. If you’re considering refinancing, it’s the amount of your loan remaining.

Step 1 — Enter the Annual Interest Rate Your loan’s annual interest rate (as a percentage). If two or more offers are running, use each one individually to see if any offer provides a lower overall cost.

Step 3 — Select Your Loan Term Common options are 5, 10, 15, 20, or 30 years. The longer the term the lower the monthly payment, but the more interest that is paid over the term. This trade-off is apparent on the calculator.

Step 4 — Add Extra Payments (Optional but Recommended), you should start with $100 or $200 more, and see how much it will save you. It’s that number that gets a lot of folks to look at their extra payment budget.

Step 5 — Click on calculate to generate the Schedule. Look at three numbers: Monthly payment, Total Interest, and Years to payoff. The three figures are all that’s needed to tell the whole story of a loan.

Step 6 — Scroll Through the Amortization Table. See your year 5, year 10, year 15 and understand your balance and equity. This is the information which drives refinancing decisions, timing of sales and planning of payoff.

Why Total Interest Matters More Than Monthly Payment

The most common error that I see and it is a costly one.

The longer a loan, the less you will have to pay each month. That’s a good feeling. However, it significantly raises the total interest paid as you are giving the lender more time to accumulate interest on the remaining amount.

Example: $200,000 personal loan at 7%

| Loan Term | Monthly Payment | Total Interest | Total Cost |

|---|---|---|---|

| 5 years | $3,960 | $37,600 | $237,600 |

| 10 years | $2,322 | $78,640 | $278,640 |

| 20 years | $1,551 | $172,240 | $372,240 |

Same loan amount. Same interest rate. The 20-year term will pay $134,640 more in interest over the 5-year term. Monthly payment difference: $2,409. Total interest difference: $134,640.

The calculator instantly does this. It will take 30 seconds to run. It can cost you hundreds of thousands of dollars not to run it.

Common Mistakes Borrowers Make

Making only the monthly payment. The numeric value that will be least meaningful on the calculator output is the monthly payment. When it comes to the bottom line, it’s total interest that tells you the actual cost of a loan.”

Failure to run additional payment scenarios. If you never pay more, it’s nice to have some idea of what that extra $100 or $200 would buy you. This calculation is done by most and they find the extra payment.

Selecting the longest term without making any effort. Longer terms are safer because they have lower payments. However, those additional years accumulate interest that is actual cash that is taken out of your account for good.

Not shopping around for loan offers side by side. Two offers for loans with different rates or terms can still cost tens of thousands of dollars in interest paid over the loan’s life. It takes around five minutes to perform both in the amortization calculator and it will show which one is the better offer.

Say goodbye to balloon payments. If you have a balloon loan, and you haven’t determined what the balloon will be, then you have an unexpected expense on your hands. Be sure to run the balloon payment calculator first before signing.

Who Should Be Using This Calculator

This is for home buyers and should be done before and not after an offer is made. Understand the full expense of the loan prior to agreeing.

Homeowners who are looking into refinancing – compare the remaining schedule for your current loan with the schedule for your refinanced loan. The calculator tells you precisely if refinancing will save you money on your intended holding period.

Car buyers – check with the dealer and base financing options with the bank/credit union. The monthly difference payment is not the only consideration.

Business owners – amortization of commercial loans is the same as it is for personal loans. Understand the repayment terms prior to signing equipment or expansion loans.

Personal loan borrowers — short-term personal loans have high interest rates that may seem affordable on a monthly basis, but can be costly in the long run. Read the full amount before you take out a loan.

Financial planners and advisors — share with clients the true expenses of debt and the true benefits of additional payments using the schedule. Explicit explanations do not have the same effect as numbers on a screen.

Frequently Asked Questions

An amortization calculator is used for?

It will show you your exact monthly loan payment, how much interest there will be on your loan and a complete amortization schedule of your loan which will break down each payment into principal and interest. It is applied in mortgages, auto loans, personal loans and business financing.

An amortization schedule is what?

A full list of all payments throughout the life of the loan – payment number, total payment amount, principal/interest portion of each payment, remaining balance after each payment. This is the most comprehensive breakdown of a loan’s actual working over time.

What impact will additional payments have on my loan?

Any extra payments are applied directly to the principal. The lower the principal, the less interest that will be charged in future months. Small increases in repayments at the start of the loan that reduce interest can save a huge amount of interest and years off the loan.

What’s the difference between fixed and variable rate amortization?

If it’s a fixed rate loan, then the amortization schedule is entirely predictable — you’ll know what each future payment is from day one. For variable rate loans, the schedule will adjust every time the rate goes up or down. Use the calculator to see how much you will be paying at your current rate and how much you will be paying at a higher scenario rate, to see your payment risk.

Is this usable for mortgage uses?

Yes — one of the major use cases is mortgage amortisation. Simply input your loan amount, mortgage rate and term to view monthly payments, total interest paid and your complete mortgage amortization schedule. This additional payment option is especially beneficial for mortgage planning.

Auto & Personal Loans are supported by the calculator?

Yes. The same calculator can be used for any amortized loan, whether it’s an auto, a personal, home equity or commercial loan. The type of loan would not affect the calculations, only the amount and the terms.

Does the calculator cost anything or is it available for free?

Yes, absolutely and totally free – no sign up or account required.

Final Thoughts

One of the biggest financial decisions people make is to go and take out a loan. The number you can fit into your budget is the monthly payment. The number that determines the “actual” cost is the total interest.

Both of these numbers are made available to you, and so are all payments in between, by using an Amortization Calculator, so you’re not making borrowing decisions with information half-shared.

Run it before taking out any loan. If you aren’t certain that you can commit, run the extra payment scenario anyway. Shop around for all offers. Examine the amortization schedule and determine how much you expect your balance to be after five years and ten years.

All this requires about a couple minutes. The price of NOT doing it can amount to tens of thousands of dollars over the life of a loan.

Here’s the calculator. The numbers appear at once. It’s up to you to use them.

About the Author

For more than 10 years, Marcus Webb has been assisting people and families with the cost of personal finance and mortgage planning before they make a commitment. He’s studied hundreds of loan agreements, refinancing situations and amortization schedules, and writes about making decisions on a loan in a state of full information, not half information.